partners for life

Aged Care Financial Advice

Gain Clarity, Confidence, and Peace of Mind

Are you overwhelmed by the prospect of navigating the Aged Care system, for yourself or a loved one? Unsure about the costs and how they will impact your Centrelink payments? Wondering how to ensure your legacy is protected while securing the best care? McKinley Plowman’s Aged Care Financial Advice service is here to address those concerns and more, and ultimately provide peace of mind.

Our Aged Care specialists understand the vast and complex considerations that come with this stage of life. We will help you navigate with clarity and confidence the financial impacts of Aged Care services and their associated fees on things like Centrelink payments, your desired lifestyle, and legacy aspirations. We take the time to understand each unique situation and financial position, identify options, outline the costs of appropriate Aged Care services, and guide you through the entire process.

Personalised Assistance for Your Unique Situation

Our specialists are dedicated to helping you and your loved ones navigate the various processes and potential pitfalls of accessing Aged Care. It’s never too early to start planning for your later years.

If you’re seeking aged care advice on behalf of a loved one, we can assist with that too. As they start to consider their aged care options, the transition can seem overwhelming. During this difficult time, filling out forms or obtaining documents may be the last thing anyone wants to do. Your financial adviser can help ensure your loved one’s needs, both financial and emotional, are fully considered.

Comprehensive Financial Guidance

Our Aged Care Advice service starts with an initial discussion, where we seek to understand your unique circumstances (or those of your loved one who requires advice). Following that initial discussion, we can assist with various strategies and considerations, including but not limited to:

- Upfront Costs: Determining applicable accommodation payments and how to fund that cost, whether through a lump sum, periodic payments, or a combination of both.

- Keeping or Selling the Home: Advising on whether to keep or sell an existing home, and the subsequent implications for Age Pension entitlements and means tests, and ongoing care costs.

- Maximising Benefits: Recommending investments to maximise Age Pension entitlements and ensuring sufficient cash flow to meet ongoing care costs.

- Estate Planning: Identifying assets for the estate and ensuring relevant beneficiary nominations are made.

- Tax Considerations: Reviewing tax offsets, including low income and seniors and pensioners tax offsets, and addressing issues like land tax and capital gains tax where applicable.

In addition to the above, our advisers work closely with estate planning professionals to ensure that your estate is distributed according to your wishes when you pass on. Effective estate planning considers who assets are distributed to, as well as seeking to do so in as tax-effective a manner as possible. Much like aged care advice, making these arrangements well ahead of time is advisable.

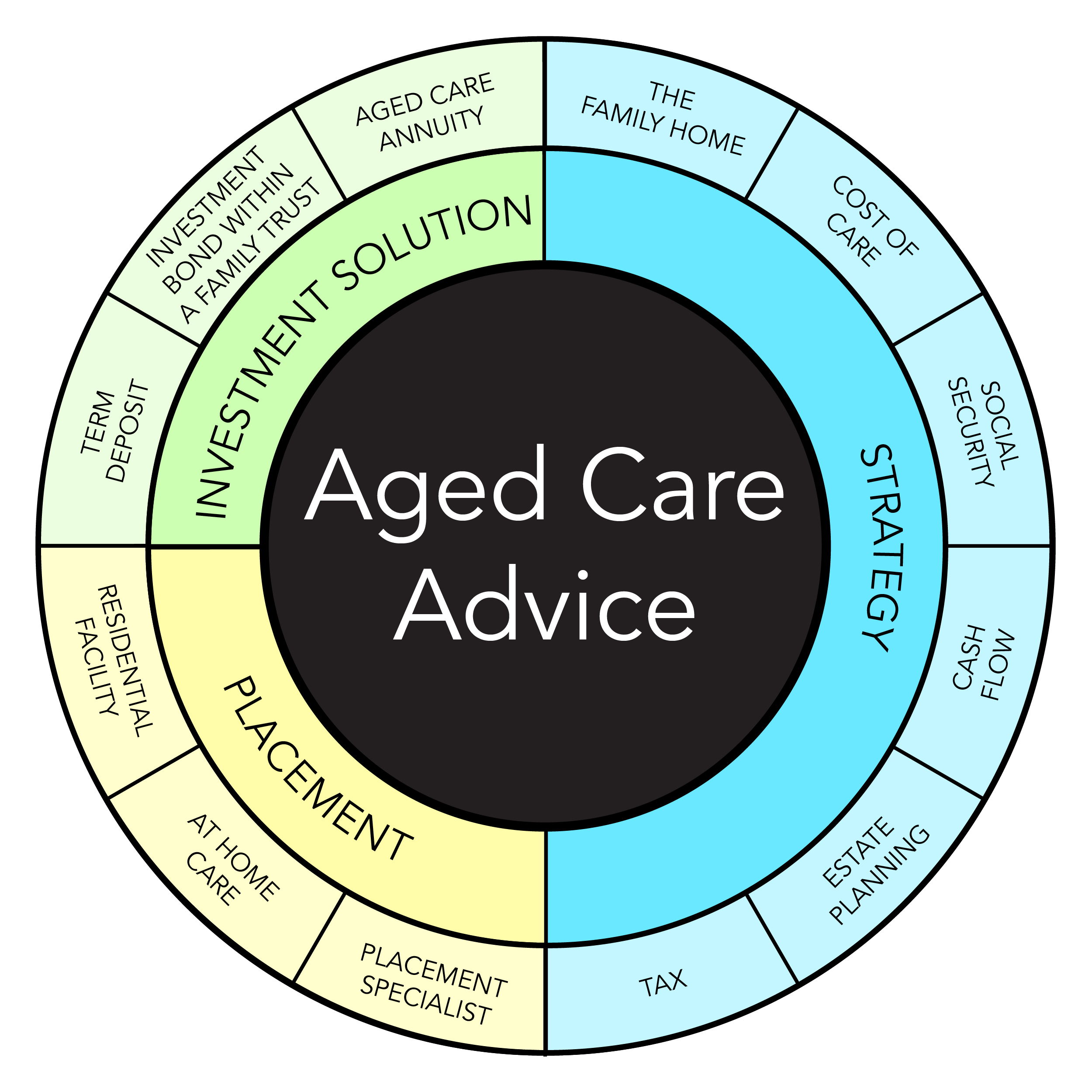

Aged Care Financial Advice – Simplifying Complexity

There are a number of considerations that must be made when planning for Aged Care. Below is an overview of the various aspect we take into account when conducting Aged Care advice – as you can see there is a lot that goes into it and it’s easy to see why people that go it alone can find themselves overwhelmed.

At McKinley Plowman, the value of our service is in simplifying and streamlining the transition to Aged Care. We leverage the experience of our in-house specialists and network of professionals to ensure every client is looked after, and all applicable avenues are explored. But don’t just take our word for it – hear from a few of our Aged Care advice clients below:

Client Testimonial 1:

After my wife developed Alzheimer’s disease, the subsequent dementia meant that she needed full time care in an aged care facility. After several less-than-positive personal enquiries to aged care facilities, I engaged McKinley Plowman to assist. The MP+ team helped clarify the financial situation that we faced and proposed a solution that has worked well for us both. They explained our options and ensured we had a plan in place to take care of the transition to Aged Care.

Following that, MercyCare Joondalup were very helpful in explaining how their side of the process worked, and took us on a tour of the facility. From there, I was able to work alongside MP+ and MercyCare to put our plan into practice. My wife was reluctant to move to the home but it was necessary for her own wellbeing. For me, a load was lifted and although it was a very emotional time for both of us, everything proceeded smoothly. I feel that MP+ took a lot of the ‘heavy lifting’ out of our situation, and freed me up to concentrate on my wife’s welfare. The outcome was an affordable and straightforward solution – while difficult at first, everything eventually settled down and life has normalised for both of us.

I would most definitely recommend McKinley Plowman’s Aged Care Advice services to others.

Clive Nealon

Client Testimonial 2:

I have been a tax and financial planning client of McKinley Plowman’s for around 15 years, so when I needed assistance to manage my father’s finances in early 2024, I turned to MP+. As he had recently moved into an Aged Care facility, we sought advice on the best way to manage his assets and ensure regular cashflow. The team at MP+ delivered timely and sound advice on optimising dad’s financial situation, and we now have the peace of mind knowing his assets are protected, his tax liabilities have been reduced, and he receives a monthly annuity payment.

The MP+ team have been professional all the way through, had the knowledge to answer all of my queries, and ultimately we are very satisfied with the outcome. I would recommend MP+ Aged Care Advice services to anyone in a similar situation.

Andy Clayton

Your Aged Care Advice Journey

If you or a loved one are considering your aged care options, seeking advice early is important. To arrange a complimentary consultation with one of our Aged Care advice specialists, please contact us on 08 9301 2200, or via our website.